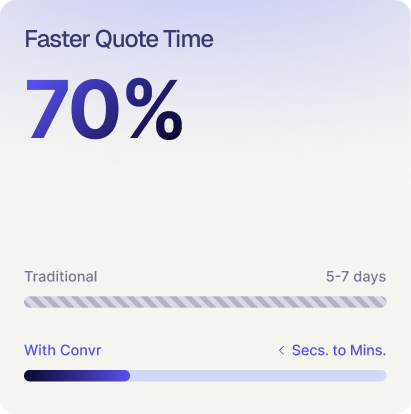

Insurance underwriting still begins with a familiar bottleneck: the submission. A broker sends a bundle of documents, emails, spreadsheets, and attachments that describe an account, and the carrier or MGA must turn that bundle into structured data that can be evaluated, priced, and quoted. The challenge is not that the information is missing. It is that it is scattered, duplicated, inconsistently formatted, and mixed with narrative descriptions that are hard to compare across accounts. A single submission can include dozens of data points that matter to risk selection and pricing, plus supporting context that helps an underwriter understand operations, controls, and loss drivers.

AI changes the nature of this work by treating submission intake as a data engineering problem rather than a manual reading task. Instead of relying on someone to interpret every field and retype it into systems, AI can extract key entities and attributes, normalize them to standard definitions, and present them as a coherent risk profile with traceability back to the original source. That shift makes it possible to move faster while improving consistency, because the same extraction logic can be applied across different document types, formats, and lines of business. The most effective implementations combine document understanding, classification, and validation so the results are not just fast, but also trustworthy enough for real underwriting decisions.

What Counts as an Insurance Submission and Where the Data Lives

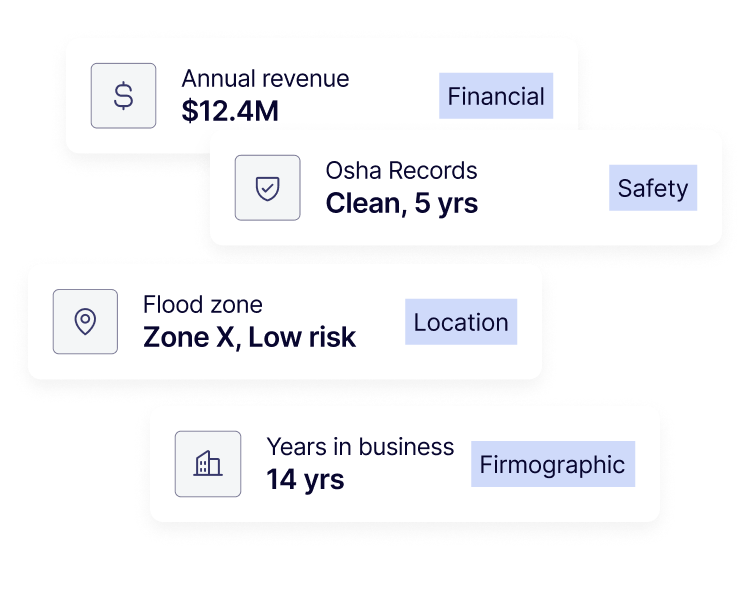

An insurance submission is best understood as the complete set of materials used to evaluate and quote a risk, not just a single form. Depending on the line and distribution channel, a submission may include an ACORD application, supplemental questionnaires, schedules of values, loss runs, prior policies, inspection reports, financial statements, driver lists, certificates, and a long email thread that clarifies open questions. It often contains documents that were originally created for other purposes, like payroll reports or lease agreements, but that carry underwriting signals.

The data in a submission lives in multiple “containers.” Some is already structured, like spreadsheet schedules or ACORD XML. Some is semi-structured, like PDFs with tables, checkboxes, and repeated labels. Some is unstructured narrative text, like a broker email describing operations, upcoming changes, or past incidents. Attachments can be scanned images, which adds the complication of OCR quality and skewed or noisy pages. Even when a PDF looks digital, it may be a flattened image with no selectable text.

Submissions also contain competing versions of the truth. A value might appear in a narrative, a questionnaire, and a schedule, each with a slightly different number or effective date. Business descriptions vary by writer and can drift away from the classification codes used by underwriting rules and rating. Locations, payroll, revenue, and vehicle counts may be given as ranges, estimates, or totals that do not reconcile across documents. The underwriting task is to reconcile these conflicts, determine what is current, and capture the data needed for appetite, triage, pricing inputs, and referral decisions.

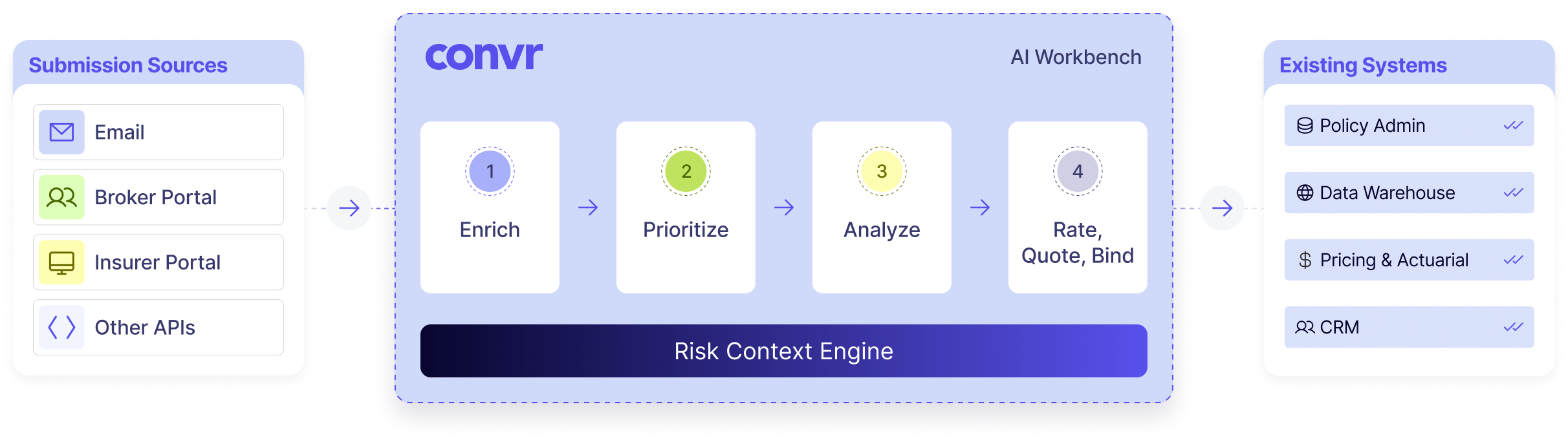

AI-assisted intake starts by recognizing that the submission is a dataset distributed across documents. The goal is to turn that distributed dataset into a single structured representation of the account, with clear source attribution and confidence, so downstream workflows can run reliably.

How AI Extracts and Structures Data From Submission Documents

AI extraction typically begins with ingestion and document organization. Files arrive through email, portals, or APIs, and the system must group them into a single submission, deduplicate, and identify document types. Document classification models look at layout, text cues, and metadata to label files as ACORD forms, loss runs, schedules, questionnaires, or correspondence. Accurate classification matters because it selects the right extraction strategy, such as table parsing for schedules or entity extraction for narrative text.

Next comes text acquisition. For digital PDFs, text can be extracted directly. For scanned documents, OCR is used to convert images into text while preserving layout coordinates. Modern OCR pipelines also detect page rotation, columns, headers, and tables, and they output tokens with bounding boxes. Those layout signals are crucial because many underwriting fields are defined by their position relative to labels and table structure, not just by the words themselves.

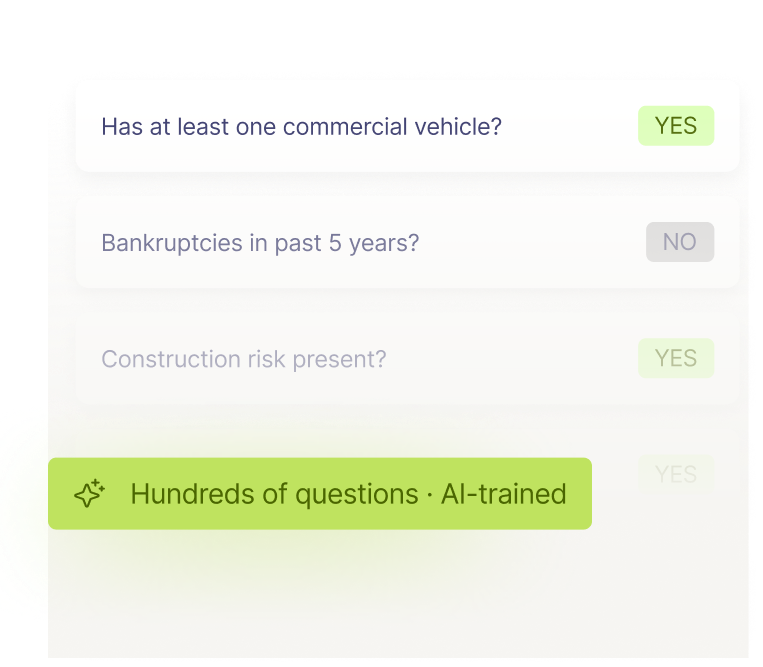

With text and layout available, AI models extract entities and attributes. There are two common approaches that are often combined. One is key-value extraction, which finds labeled fields like “FEIN,” “Years in business,” or “Total payroll” and captures the corresponding value. The other is semantic extraction, which identifies entities like named insured, locations, operations, building details, limits, deductibles, and loss events, even when the document does not use consistent labels. Table understanding is a specialized capability that extracts rows and columns from schedules of vehicles, properties, or equipment while preserving relationships like per-item value and address.

Structuring is where the biggest payoff happens. Extracted values must be normalized into canonical formats: dates standardized, currencies parsed, addresses validated, units reconciled, and totals computed. Business descriptions can be mapped to standardized classifications used for underwriting rules and rating. When the system is powered by an insurance-specific ontology, it can represent the account as a graph of related objects, such as a policy period with coverages, a set of locations with exposures, and operational attributes that drive risk scoring. That structure supports downstream automation like appetite checks, rule-based referrals, and prefill into rating systems.

Finally, a practical extraction system generates an “evidence layer.” Every extracted value should carry provenance such as document name, page number, and highlighted text region, plus a confidence score and any conflicts detected across sources. That evidence is what allows underwriters to trust the output and quickly verify or correct it.

Validation, Auditability, and Regulatory Considerations for AI-Extracted Submission Data

Extracted submission data is only useful if it can be trusted, explained, and reviewed. Validation is the set of checks that ensure extracted fields are plausible, consistent, and aligned with underwriting expectations. Some checks are basic formatting, like making sure a FEIN has the right length or a date parses correctly. Others are domain-specific, like ensuring payroll totals reconcile with class code breakdowns, that building values are consistent with construction and square footage ranges, or that the number of vehicles matches a schedule count. Validation can also use cross-document logic, such as verifying that the effective date in a quote request matches the dates referenced in loss runs and prior policy declarations.

Conflict resolution is a major component of validation. When two documents disagree, the system should not silently pick one. Instead, it should surface the conflict, show the competing sources, and apply a clear rule set. Sometimes recency matters, such as preferring the most recent supplemental. Sometimes document authority matters, such as prioritizing a signed application over an email estimate. In many workflows, the best approach is to present the discrepancy and let the underwriter decide, while the system tracks the final selected value.

Auditability depends on traceability and versioning. Underwriting files evolve as brokers send updates. An AI system should retain snapshots of extracted data by submission version, track what changed, and maintain links back to the exact source excerpt that supported the value at the time of decision. This enables defensibility in post-bind reviews, claims disputes, and internal audits. It also reduces rework because renewals can be compared against prior extracted profiles to identify material changes.

Regulatory considerations are largely about governance, privacy, and fairness. Submission documents can contain sensitive personal information, and handling must comply with data minimization, access controls, retention policies, and encryption. Models should be monitored for consistent behavior, and organizations should document how AI is used in the workflow, especially where it influences decisions like triage, appetite, or pricing inputs. Human oversight remains central. AI can propose extracted values and risk indicators, but underwriting decisions should be reviewable, and the organization should be able to explain what data was used and why. Practical controls include role-based permissions, redaction of unnecessary PII, logging of model outputs and edits, and clear procedures for correcting errors.

Common Failure Modes and How Teams Mitigate Them in Underwriting Workflows

Even strong AI extraction systems fail in predictable ways. One common failure is poor input quality. Low-resolution scans, fax artifacts, skewed pages, and handwritten notes can degrade OCR and lead to missing or incorrect values. Mitigation starts with ingestion controls such as minimum quality thresholds, automatic image enhancement, and prompts to brokers when documents are unreadable. Some teams also route low-quality documents to a human-assisted capture path to prevent silent errors.

Another failure mode is document variability. The same information can appear in countless formats, and carriers often see custom broker templates. Models trained on limited templates may mislabel fields or misread tables with merged cells and multi-line headers. Teams mitigate this by combining machine learning with rules that leverage layout anchors, maintaining a library of known templates, and continuously retraining models on new examples. Active learning workflows, where corrections made by underwriters feed back into training data, can improve coverage over time.

A third failure is semantic ambiguity. Terms like “sales,” “revenue,” and “gross receipts” may be used interchangeably, but they can have different underwriting meanings. “Total insured value” might refer to building plus contents in one context and only scheduled equipment in another. Mitigation requires a domain ontology and contextual extraction, where the model uses surrounding cues, document type, and line of business to assign the right meaning. It also helps to capture units and time periods explicitly, such as annual revenue for the most recent fiscal year.

Cross-field inconsistencies can also break downstream workflows. For example, an address may be extracted incorrectly, leading to geocoding errors and misapplied territory factors. Or a deductible may be captured without noting whether it applies per occurrence or aggregate. Teams mitigate this with validation rules, reference data enrichment, and “must-verify” flags when confidence is low or when downstream impact is high.

Finally, there is workflow risk: even correct extraction can be ignored if it does not fit how underwriters work. If users cannot quickly see evidence, correct values, and understand what changed, they will revert to manual review. Mitigation is a human-centered design that emphasizes side-by-side evidence, fast editing, clear confidence indicators, and seamless export into underwriting and rating systems. The best teams treat AI as a co-pilot that reduces reading and typing, not as a black box that replaces judgment.

FAQs

How is AI different from traditional OCR and form recognition in submissions?

Traditional OCR converts images to text, and older form recognition tries to locate fields based on fixed templates. AI-based submission intake goes further by understanding both language and document structure across many formats. It can classify document types, extract entities even when labels change, and interpret relationships in tables like schedules of vehicles or locations. It also normalizes data into consistent types, such as standardizing dates, addresses, and monetary values, and it can map operations to standardized business classifications. Another key difference is evidence and confidence. A modern AI system can attach provenance like page and excerpt, and it can flag uncertain values or conflicts across documents. In practice, that means fewer brittle template dependencies, better handling of broker variability, and a workflow where underwriters review highlighted evidence instead of rekeying everything.

What kinds of submission fields are most suitable for AI extraction, and which are hardest?

Fields that are labeled, repeated, and formatted consistently tend to be easiest, such as named insured, addresses, policy dates, limits, deductibles, and many schedule columns like VIN, year, make, and value. Loss run data also works well when the table structure is clear, enabling extraction of loss dates, amounts, causes, and status. Harder fields are those that depend on interpretation, such as describing operations, identifying material changes, or determining whether a control is “adequate” based on narrative wording. Tables become difficult when they have merged cells, footnotes, or multi-level headers, or when totals are embedded in narrative rather than listed clearly. The best approach is hybrid: use AI for broad extraction and normalization, then design review checkpoints for ambiguous items with high underwriting impact.

How do teams ensure the extracted data is accurate enough to trust for quoting?

Accuracy comes from layered controls, not just one model score. Teams typically combine confidence thresholds, validation rules, and source-based verification. For example, if the system extracts a payroll figure, it can check that it is numeric, that it aligns with the sum of class code subtotals, and that it matches the time period stated in the document. When documents disagree, the system should surface the conflict with evidence, not guess silently. Underwriters also need an efficient way to confirm values, such as clicking a field to see the highlighted excerpt and adjusting it when needed. Over time, capturing those corrections and using them to retrain models improves accuracy on the specific mix of broker templates and lines of business the team sees most often.

Can AI help identify material changes at renewal from submission documents?

Yes, if the extracted submission data is structured and versioned. The core capability is comparing the prior extracted risk profile to the current one and detecting changes in exposure and operations. Examples include new locations, increases in revenue or payroll, changes in construction or occupancy, added vehicles or drivers, new products or services, or changes in safety controls. AI helps by pulling those signals from multiple documents, including emails and supplemental questionnaires, and presenting a concise change summary with evidence links. The key is to store prior-year extracted data in a consistent schema so comparisons are meaningful, and to track document provenance so an underwriter can see exactly where the change was stated. This supports faster renewal triage and reduces the risk of missing subtle but important updates.

What role does an insurance ontology play in extracting submission data?

An ontology provides a shared set of definitions and relationships that turns raw extracted text into underwriting-ready structure. Instead of storing isolated fields, the system can represent concepts like accounts, locations, coverages, exposures, loss events, and operational attributes, and how they relate. That makes normalization more consistent, such as distinguishing named insured from additional insured, separating mailing address from risk location, or associating scheduled values with the correct location and coverage. It also supports classification, such as mapping business descriptions to standardized categories used for appetite and risk scoring. When extraction is ontology-driven, downstream workflows benefit because rules, analytics, and integrations can rely on consistent meaning even when the original documents are inconsistent.

Conclusion

AI-driven extraction turns insurance submissions from a slow, manual reading exercise into a repeatable process that produces structured, validated data with clear evidence. It starts by organizing the submission, classifying documents, and converting content into machine-readable text while preserving layout. It then extracts key entities and tables, normalizes values into consistent formats, and maps them into a risk profile that underwriting systems can use. The most important ingredient is not speed alone, but trust: conflict detection, validation rules, provenance, and versioning make it possible to review, audit, and defend decisions. Just as importantly, teams reduce operational risk by designing workflows that highlight evidence, support quick corrections, and focus human attention on ambiguity rather than data entry.

Common failure modes are manageable when treated as expected realities: low-quality scans, template variability, semantic ambiguity, and cross-field inconsistencies. Mitigations like quality controls, hybrid extraction methods, ontology-driven structuring, and continuous learning from user corrections allow performance to improve over time. The result is a workflow where underwriters can move faster without losing rigor, and where renewals can be compared consistently to identify meaningful changes.

To see how a modular AI underwriting and intelligent document automation workbench approaches submission extraction with structured data, evidence, and underwriting workflow fit, visit https://convr.com/.